What Are Import Duties?

Import duties (also called customs duties or tariffs) are taxes levied by governments on goods entering their territory. In the European Union, import duties are set at the EU level and apply uniformly across all 27 member states. When you import goods into any EU country, you pay the same duty rate — whether the shipment arrives in Rotterdam, Hamburg, or Piraeus.

The revenue from import duties goes directly to the EU budget (member states retain 25% as a collection fee). But duties serve a broader purpose than revenue: they protect European manufacturers from low-cost competition, enforce trade agreements, and implement trade policy.

For importers, duties are a direct cost of doing business. A wrong classification or missed exemption can mean paying thousands of euros more than necessary — or facing penalties for underpayment.

Typical EU duty rates on manufactured goods

Distinct product codes in the EU TARIC database

Customs value basis: Cost + Insurance + Freight

How Are EU Import Duties Calculated?

The duty you pay depends on three factors. Get any of them wrong, and your calculation is off.

The HS/TARIC code of your product

Every product has a 10-digit TARIC code that determines the applicable duty rate. A wireless headphone (8518.30.00) pays 0% duty. A plastic toy (9503.00.95) pays 4.7%. The code matters enormously.

The customs value of the goods

This is the CIF value: the product cost, plus insurance, plus freight to the EU border. Not just the purchase price — transport and insurance are included in the taxable base.

The country of origin

The EU has free trade agreements and preferential tariffs with many countries. Goods from South Korea may enter at 0%, while the same product from China pays the full rate. Origin determines which rate applies.

The Basic Formula

Example: You import 500 bamboo cutting boards from China. Product cost: €2,000. Shipping: €400. Insurance: €50.

Customs value (CIF) = €2,000 + €400 + €50 = €2,450

HS code 4419.19.00 (wooden kitchenware) → duty rate: 0%

Import duty = €2,450 × 0% = €0

Note: you still pay 21% VAT over the customs value in the Netherlands, but the import duty itself is zero for this product.

Customs Value: The Basis for Your Duty

The customs value is not simply what you paid for the goods. The EU uses the transaction value method (WTO Valuation Agreement), which includes several cost components:

How Your HS Code Determines Your Duty Rate

The Harmonized System (HS) code is the single most important factor in determining how much duty you pay. Every product imported into the EU must be classified with a 10-digit TARIC code, and each code has a specific duty rate attached to it.

The difference between two seemingly similar codes can be dramatic:

| Product | HS Code | Duty Rate |

|---|---|---|

| Laptop computer | 8471.30 | 0% |

| Bluetooth speaker | 8518.22 | 0% |

| Cotton t-shirt | 6109.10 | 12% |

| Ceramic tableware | 6912.00 | 12% |

| Bicycle | 8712.00 | 14% |

| Leather shoes | 6403.99 | 8% |

| LED lighting fixture | 9405.42 | 4.7% |

Not sure which HS code applies to your product? Our AI classifies products in seconds.

Types of EU Import Duties

Not all duties are the same. The EU applies several types depending on the product and origin country.

Ad Valorem Duties (most common)

A percentage of the customs value. Example: 12% on cotton clothing. This is the most common type — about 90% of EU tariff lines use ad valorem rates.

Specific Duties

A fixed amount per unit of measurement (weight, volume, quantity). Example: €17.60 per 100 kg on certain rice imports. Common in agriculture.

Compound Duties

A combination of ad valorem and specific. Example: 8% + €2.50/kg. Used for products where both value and quantity matter, such as processed foods.

Anti-Dumping & Countervailing Duties

Extra duties on products sold below fair market value (dumping) or subsidised by foreign governments. These can be substantial — EU anti-dumping duties on Chinese e-bikes, for example, range from 18.8% to 79.3% on top of the regular duty.

Tariff-Rate Quotas (TRQs)

A lower duty rate applies up to a certain import volume; once the quota is filled, the standard (higher) rate kicks in. Common in agriculture — New Zealand butter, for example, enters at a reduced rate up to the quota limit.

CBAM surcharge on carbon-intensive goods: importers of steel, aluminium, cement and fertilisers may face an additional CO₂ levy at the EU border from 2026 onwards.

Learn about CBAMVAT on Imports

Import duty is not the only tax you pay at the border. Import VAT is charged on top of the customs value plus the duty amount. This is often the larger cost component.

Total Landing Cost Formula

Import VAT Rates Across the EU

Preferential Tariffs & Trade Agreements

The EU has free trade agreements (FTAs) with over 70 countries. If your goods originate from one of these countries and you can prove it with a certificate of origin, you may pay a reduced or zero duty rate.

EU-South Korea FTA

Nearly all industrial goods enter at 0%. One of the EU's most comprehensive trade deals.

EU-Japan EPA

Eliminated duties on most goods, including electronics and vehicles (phased).

EU-Vietnam FTA

Duty elimination on 99% of tariff lines over 7–10 years. Increasingly relevant as manufacturing shifts from China.

GSP (Generalised Scheme of Preferences)

Reduced rates for developing countries. Covers many Asian and African nations. Requires Form A or REX statement.

China — No FTA

China has no preferential agreement with the EU. All Chinese goods pay the full MFN (Most Favoured Nation) rate. This is the standard TARIC rate you see in the database. See our complete guide on importing from China for what this means in practice.

Common Duty Mistakes That Cost Money

Using the wrong HS code

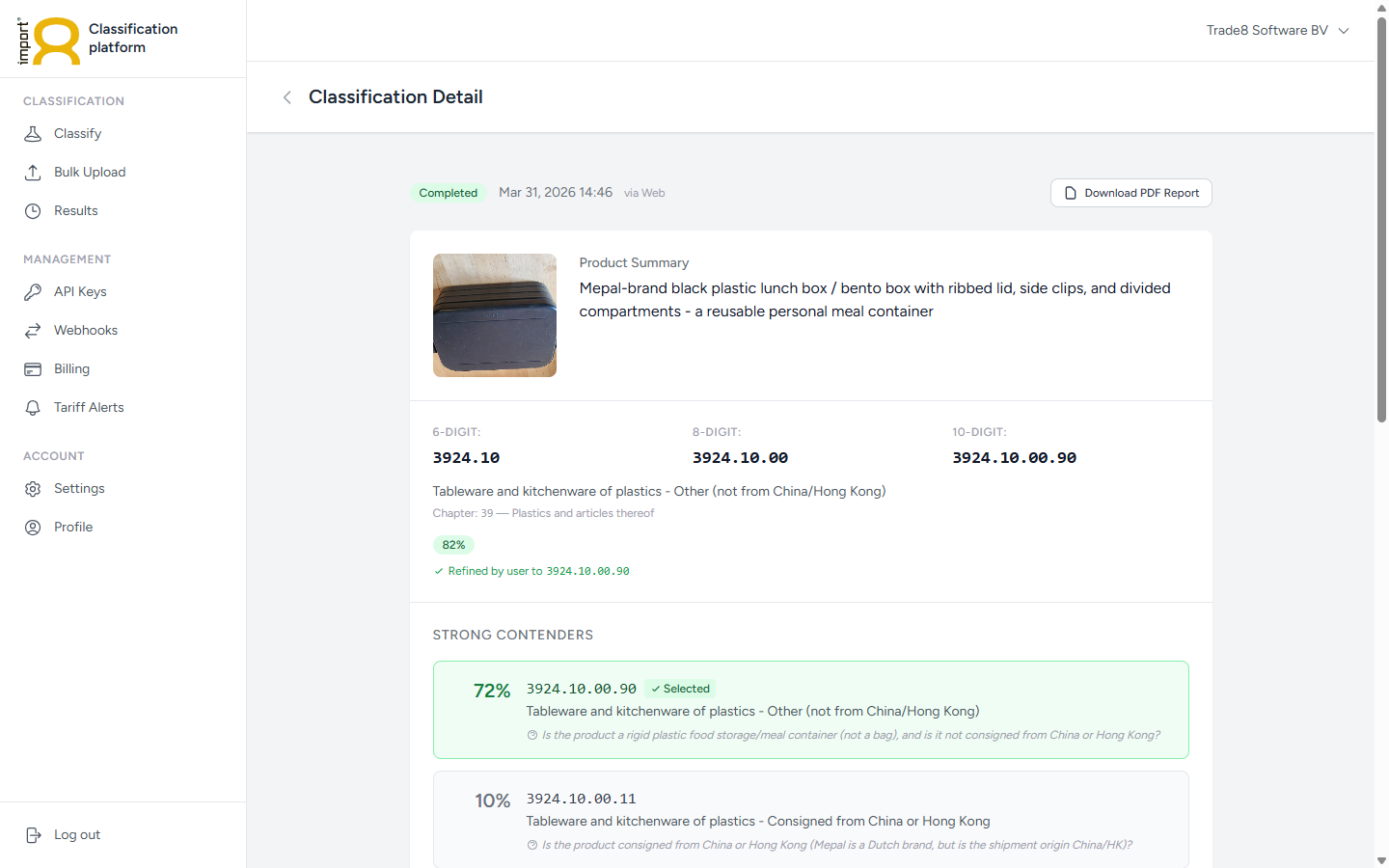

The most expensive mistake. Classifying a product under the wrong code can mean paying 12% duty instead of 0%, or facing a customs audit with back-payments and penalties. See our guide on the most common HS code mistakes to avoid.

Declaring FOB instead of CIF value

If you declare only the product cost without shipping and insurance, you're undervaluing your goods. Customs may adjust the value and charge interest on the difference. Some importers do this intentionally — it's fraud and carries serious penalties.

Missing a preferential rate

Many importers pay the full MFN rate when they could qualify for 0% under an FTA. If your supplier is in Vietnam, South Korea, or another FTA partner — check if a preferential rate exists and request the origin documentation.

Ignoring anti-dumping duties

Anti-dumping duties are on top of the regular rate and can exceed 50%. They apply to specific products from specific countries — and they change regularly. If you import steel, aluminium, ceramics, solar panels, or e-bikes from China, always check the current anti-dumping measures.

Not budgeting for duties upfront

Import duty + VAT can add 25–40% to your landed cost. If you don't factor this into your pricing model before ordering, your margins evaporate. Always calculate duties before you commit to a purchase order.

How to Calculate Your Import Duties

Here's a step-by-step process for calculating what you'll pay at the EU border.

Step 1: Classify your product

Find the correct HS/TARIC code. This determines everything. Start with our guide on how HS codes work, search the TARIC database manually, or use an AI classification tool to get results in seconds. Validate your classification with the free HS Code Sanity Check.

Step 2: Determine the origin country

Not the country you're buying from — the country where the goods were manufactured or substantially transformed. This determines if preferential rates apply.

Step 3: Look up the duty rate

Search for your TARIC code + origin country in the TARIC database. You'll see the MFN rate (standard) and any applicable preferential rate, anti-dumping duty, or trade measures.

Step 4: Calculate the customs value

Add up: product cost + shipping + insurance = CIF value. Convert to EUR if needed.

Step 5: Apply the rate

Duty = customs value × duty rate. Then add import VAT on top of (customs value + duty). That's your total cost at the border.

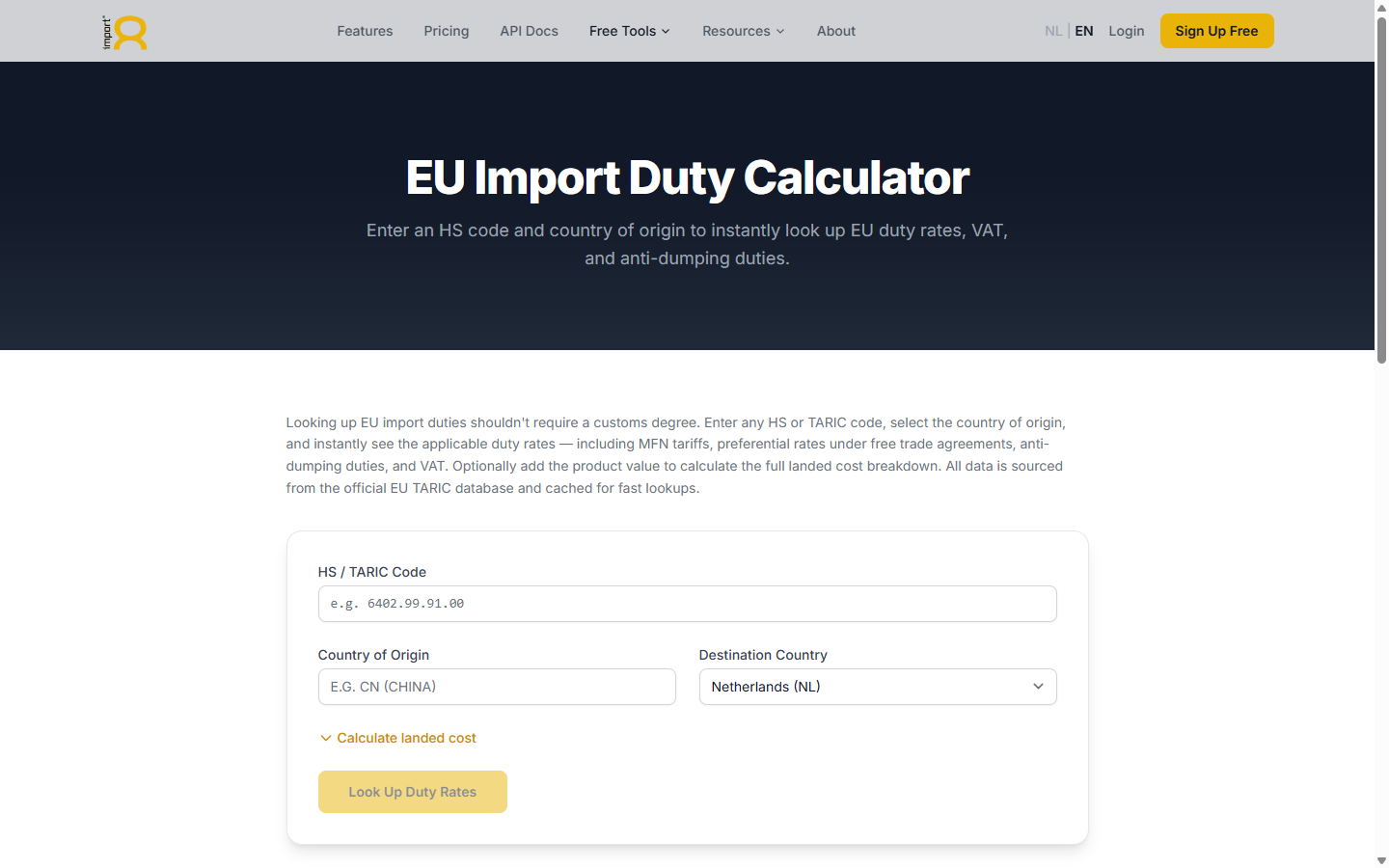

Skip the manual calculation

Our free EU Import Duty Calculator does steps 3–5 automatically.

Frequently Asked Questions

Not always. Some products have a 0% duty rate (e.g., most electronics under the ITA agreement). Small consignments under €150 are exempt from customs duty (but not VAT). And goods from FTA partner countries may enter duty-free with proper origin documentation.

Customs duty is a tax based on the product classification and origin, payable to the EU. Import VAT is a national tax (like the Dutch 21% BTW) charged on the customs value plus the duty. For VAT-registered businesses, import VAT is deductible; customs duty is not.

Yes, in certain cases. If you overpaid due to a classification error, you can apply for a refund within 3 years. If goods are re-exported, defective, or don't match the order, you may also qualify. The process goes through your national customs authority (e.g., Douane in the Netherlands).

First, determine the correct HS/TARIC code for your product. Then look it up in the EU's TARIC database (ec.europa.eu) with the origin country. The database shows the applicable MFN rate, preferential rates, and any additional measures. Or use our free Duty Calculator to get the rate instantly.

If customs discovers a wrong classification, you may owe back-duties for up to 3 years of previous imports under that code. Penalties can range from the duty difference to significant fines. In serious cases (intentional misclassification), it's treated as customs fraud. Getting the code right the first time is always cheaper than correcting it later.

Yes. Commercial shipments with a customs value under €150 are exempt from import duty (but import VAT still applies from the first euro since July 2021). Genuine trade samples of negligible value may also be exempt. Goods temporarily imported for exhibitions or testing can use the Temporary Admission procedure to avoid duties altogether.